Last updated May 8, 2026

6 min read

Architecture Review Before a Fundraising Round: What to Fix Before Investors Ask

Investors do not need your codebase to be perfect. They need your team to understand what it has built.

An architecture review before a fundraising round gives you a senior outside view of your codebase, system design, deployment process, documentation, and technical risks before investor technical due diligence begins. The goal is not to hide debt. The goal is to know the debt, explain the trade-offs, and show a credible plan before someone else frames the story for you.

That matters because technical diligence usually tests the story behind the product. A pitch deck says the platform can scale. The codebase shows whether that claim is true, partly true, or dependent on one engineer who has kept the whole system in their head since the MVP.

Fundraising turns technical debt into business risk

Before a round, technical debt can feel like an engineering problem. After a term sheet, it becomes an investor question.

Mr. CTO’s 2026 Series A diligence guide frames the issue well: investors are not grading every startup against a perfect architecture. They are asking whether the technical maturity matches the business maturity and valuation. A seed-stage product can carry rough edges. A Series A product with enterprise customers, no staging environment, and one person who understands deployment looks different.

The risk is not having technical debt. The risk is being surprised by it.

An architecture review gives you a controlled version of the questions investors are likely to ask. Can the system handle 10x current load? What breaks first? Which parts of the codebase are hardest to change? How quickly could a new engineer become useful? Where does user data live? What happens if the original developer leaves?

Those questions are uncomfortable. They are also useful before the round, when you still have time to answer them with evidence instead of improvisation.

What an architecture review should cover before investor diligence

A fundraising-oriented review should not become a generic code critique. It should focus on the parts of the system that affect investor confidence, roadmap risk, and post-funding execution.

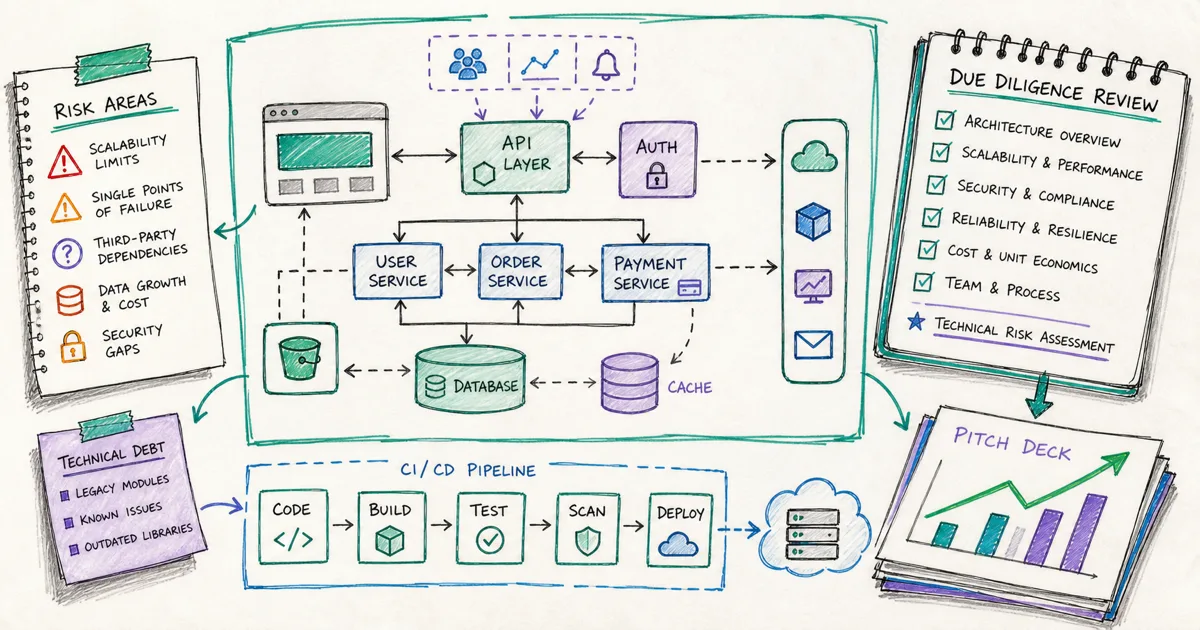

Kompella Technologies’ 2026 technical due diligence checklist uses a similar seven-area lens, covering architecture, code quality, infrastructure, security, team knowledge, product data, and operational maturity. That is the right shape. A founder does not need a theatrical audit. You need a plain technical map that helps you answer investor questions with calm detail.

The strongest deliverable is usually short: a risk register, a system diagram, a remediation roadmap, and a one-page technical summary you can use in diligence conversations.

The best time to run the review is earlier than you think

If you start the review after investors request diligence access, you are already reacting. You may still learn useful things, but you have lost the chance to fix the highest-risk items before the conversation.

| Timing | What the review can change | What it cannot change |

|---|---|---|

| 6 months before raise | Critical fixes, test coverage, documentation, roadmap framing | Historical architecture choices |

| 3 months before raise | Technical summary, risk register, dependency cleanup, focused refactors | Large platform migrations |

| 1 month before raise | Diligence prep, answer rehearsal, known-risk narrative | Meaningful architecture repair |

| During diligence | Clarification and evidence | The investor’s first impression |

The practical target is three months before active fundraising. That leaves enough time to document the architecture, clean up exposed credentials, reduce obvious dependency risk, add tests around critical workflows, and prepare the technical narrative. Six months is better if you already suspect the codebase has deep scaling or maintainability problems.

One month is still useful, but it changes the nature of the work. At that point, the review is less about fixing the system and more about knowing exactly what you are walking into.

The review should make your trade-offs easier to explain

Early products contain shortcuts. That is normal. The difference between a reasonable shortcut and a diligence red flag is whether the team can explain why the decision was made, what risk it creates, and how it will be corrected.

Weak answer “The agency built it this way and it works for now.” This makes the investor wonder who owns the system, whether anyone understands it, and whether the product will absorb the next stage of growth.

Stronger answer “We kept checkout and billing in the monolith because transaction volume was low. The review found that reporting queries now compete with critical writes, so the post-round plan moves reporting to a read model first.”

The second answer is not pretending the architecture is perfect. It shows judgment. It names the trade-off. It connects technical work to business growth.

That is what an architecture review should give you: language, evidence, and priority. You should be able to tell an investor which risks matter, which ones do not, and which ones are already scheduled.

Red flags to find before someone else finds them

Some architecture issues are normal stage debt. Others make investors slow down because they suggest the product cannot absorb capital safely.

A recent founder discussion on Reddit captured the anxiety behind this search: a team preparing for a first round had Node, Postgres, and AWS, but worried that quick product decisions and weak documentation would not hold up under a serious review. The community answer was consistent with investor-side diligence writing: imperfect code is less alarming than hidden complexity and decisions nobody can explain.

That is the real job of the review. It turns hidden risk into known risk. Known risk can be prioritised. Hidden risk becomes someone else’s objection.

Frequently Asked Questions

Do we need an architecture review before every fundraising round?

No. You need one when the round depends on technical confidence: a new product stage, enterprise customers, regulated data, a larger engineering team, or a story about scale. If the product is still a prototype with limited usage, a lighter technical readiness review may be enough.

How long before fundraising should we run the review?

Three months before active investor conversations is a practical minimum. Six months is better if you already know there are deep architecture or documentation problems. One month before the round still helps, but it mostly prepares your answers rather than changing the system.

Will an architecture review scare investors if it finds problems?

The review itself does not scare investors. Surprise does. A clear review helps you say, "We know the risk, here is the plan, and here is what changes after the round." That is stronger than waiting for an investor's technical advisor to discover the same issue first.

What will investors look for in technical due diligence?

Common areas include architecture, scalability, security, test coverage, deployment process, documentation, team knowledge, dependency risk, and whether the technical roadmap supports the business plan. The exact depth depends on stage, sector, and investor sophistication.

Can our CTO run the review internally?

Your CTO should be involved, but an outside review is useful because it tests the system without internal assumptions. The reviewer asks basic questions your team may have stopped asking and can spot where the codebase contradicts the fundraising story.

What should the final deliverable include?

For fundraising, the useful deliverables are a short architecture report, a risk register, a system diagram, a remediation roadmap, and a one-page technical summary. A long slide deck is less useful than clear answers the founder and CTO can use in diligence.

What next?

If your next raise depends on proving that the product can carry the next stage of growth, start with a review before the investor process starts. The point is not to polish the codebase for show. The point is to understand it well enough to defend the plan.